Twenty-plus years ago, I attended one of the Animation Guild's Golden Awards banquet, a ceremony where TAG celebrates artists who have worked fifty years (or close to) in the cartoon biz. While I was standing in the restaurant foyer congratulating a recipient on his fifty years, Disney veteran Joe Hale walked up and said: "Fifty years? This is the only business where you

have to work fifty years. To

survive..."

Two decades further on, I've come to see what Joe meant...

The animation business can be cold, cruel and abrupt. You're cruising along earning a good salary, happy with your job, thinking it's going to go on forever (or at least until next March) when you get called into a group meeting and told the project's shutting down and everyone will be laid off on Friday (except for Doris the production manager, who's "family.")

And suddenly you're out of work and scrambling. Two weeks before your unemployment runs out, you land another gig at a smaller studio for three hundred less per week, but you're happy to get it. You dig in and give the job your all. And eight months later, the job ends and you're looking for work again.

This, with some variations and exceptions, is the animation industry as many of us know it. Big salaries morph to smaller salaries. Long-term staff employment is followed by a year of free-lance work, then staff work opens up again and wages creep up a bit.

Through it all, lots of artists live paycheck to paycheck. And the thing I've noticed, lots of artists live paycheck to paycheck no matter how much they're making. I knew an animator at Disney who got laid off in the Great Bloodletting of 2002, when the last of the traditional animation staff was given its walking papers. He'd worked at Disney for over twenty years, made sizable bonuses, made big money in the last nine or ten years of his tenure. And within six months of layoff, finding no work, he was forced to sell his house (which was not small.)

Now, this is crappy, no question about it. But my question is, why would somebody who made steady money for two-plus decades, and beaucoup dollars for the last ten years, have to bail out of his domicile within months? A friend of his told me: "When Bill made more bucks, he spent more bucks. He had a Lexus, he had a monster-size house, he had a collection of artwork and rare comic books and lots of pictures of his trips to Europe. What he didn't have was a bank account."

It's a story I've heard a lot in the course of doing this job. When artists are in the chips, they cash in the red ones, the white ones, the blue ones, and party hearty. And when they're shut out of a place at the table, they have nothing in their metaphorical wallets on which to live. As a supervisor at DreamWorks said five years ago: "I drive a beat-up old Buick. Most of the people in my department are driving Jags and BMWs. They think the big salaries are the normal deal, no matter what I tell them."

Five years later, some of those people are surviving on smaller weekly paychecks in smaller places. Some are out of the business altogether. And renting.

Mind you, I don't wag my wizened finger at any of these folks. Twenty years back, I was just like them. I chased rainbows, I didn't save. I assumed, thirty-year-old idiot that I was, that next week would take care of itself. Now, of course, standing in the wide, sunlit uplands of Wisdom and Total Insight, I can look back at the twisting road behind me and see with crystal clarity the choices I should have made, the investments into which I should have put disposable income.

The reasons I bring this up now is, 1) the American savings rate is below zero, 2) saving is relatively painless if you're smart about it (and we don't necessarily have to mimic the American savings rate), and 3) when you reach middle age, you are going to wish like hell you had some cushion of savings to bounce along on.

The first order of business is to start saving. Put something into a 401(k) Plan (the Feds give you a tax break now to do it), then a Roth-IRA (the Feds give you a tax break later), then a certificate of deposit (the Feds give you nothing, but put the money aside anyway). Fund your accounts automatically, on the day you get paid. Set aside a percentage. Pretend the money isn't there.

Learn something about making investments. It isn't particularly hard, and if you're smart about it, the task won't take big amounts of time. Yesterday in the Wall Street Journal there was a column touting investment books; we give you three that are quite good below (two of the three are quick reads):

"Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor," by John Bogle (John Wiley and Sons, Inc.) This book from the former Vanguard chief provides good basics on how to think about mutual fund investing. Mr. Bogle, naturally, favors the indexing strategy that made Vanguard famous, while touching on other aspects of fund investing such as long-term planning, asset allocation and proper risk taking.

The Intelligent Investor Revised Edition," by Benjamin Graham and Jason Zweig. (Collins Business Essentials.) Mr. Graham is famous for his book "Security Analysis," considered the bible of value investing. This book takes a more Main Street approach and provides excellent pointers on how to approach investing. Warren Buffett is one of the many Graham admirers in the investment firmament. Mr. Zweig, a Money Magazine writer, updates this classic with modern examples that outline Mr. Graham's still salient points.

The Little Book that Beats the Market," by Joel Greenblatt (Wiley). If you are looking for a quick investing read, this is for you, since it is, in fact, little. Mr. Greenblatt, a successful hedge fund manager, provides a sharply written, anecdote rich, easy-to-understand investing strategy that any junior high-schooler would understand. While the book boasts a "magic formula," it is basically a reiteration of an age-old theme: Smart investors buy good companies cheaply...

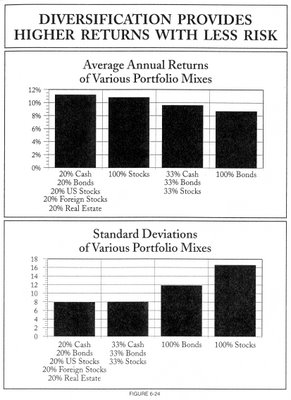

A book that I found real useful is a volume titled The Truth About Money," by Ric Edelman. He pretty much covers everything about the long green that you'll need to know, and he's simple, clear and direct, plus his investment tips are good. (We give you one of his investment charts to the left -- which is self-explanatory, I think. DI-VERS-IFY)

The point is, no matter where you are with your career, you need to pay attention to saving for retirement (And to what you've already got. Cases in point: In the last couple of months, I've encountered several animation artists who've worked fifteen-plus years in signator shops that were astounded to learn that they get TWO pensions automatically. Most kew about the monthly benefit check they get, but they didn't know they get a BIG retirement lump-sum payment when they retire called The Individual Account Plan. They were delighted they had sixty thousand dollars sitting in an account in their name. I was surprised they didn't know...)

Moral of the story: start saving early. Even if it's a pittance, be consistent about it. By the time you reach fifty or sixty, you won't be worrying about what you'll do for eating money when your last employer waves you out the door into the waiting arms of Social Security.

A book that I found real useful is a volume titled The Truth About Money," by Ric Edelman. He pretty much covers everything about the long green that you'll need to know, and he's simple, clear and direct, plus his investment tips are good. (We give you one of his investment charts to the left -- which is self-explanatory, I think. DI-VERS-IFY)

The point is, no matter where you are with your career, you need to pay attention to saving for retirement (And to what you've already got. Cases in point: In the last couple of months, I've encountered several animation artists who've worked fifteen-plus years in signator shops that were astounded to learn that they get TWO pensions automatically. Most kew about the monthly benefit check they get, but they didn't know they get a BIG retirement lump-sum payment when they retire called The Individual Account Plan. They were delighted they had sixty thousand dollars sitting in an account in their name. I was surprised they didn't know...)

Moral of the story: start saving early. Even if it's a pittance, be consistent about it. By the time you reach fifty or sixty, you won't be worrying about what you'll do for eating money when your last employer waves you out the door into the waiting arms of Social Security.

Twenty-plus years ago, I attended one of the Animation Guild's Golden Awards banquet, a ceremony where TAG celebrates artists who have worked fifty years (or close to) in the cartoon biz. While I was standing in the restaurant foyer congratulating a recipient on his fifty years, Disney veteran Joe Hale walked up and said: "Fifty years? This is the only business where you have to work fifty years. To survive..."

Two decades further on, I've come to see what Joe meant...

The animation business can be cold, cruel and abrupt. You're cruising along earning a good salary, happy with your job, thinking it's going to go on forever (or at least until next March) when you get called into a group meeting and told the project's shutting down and everyone will be laid off on Friday (except for Doris the production manager, who's "family.")

And suddenly you're out of work and scrambling. Two weeks before your unemployment runs out, you land another gig at a smaller studio for three hundred less per week, but you're happy to get it. You dig in and give the job your all. And eight months later, the job ends and you're looking for work again.

This, with some variations and exceptions, is the animation industry as many of us know it. Big salaries morph to smaller salaries. Long-term staff employment is followed by a year of free-lance work, then staff work opens up again and wages creep up a bit.

Through it all, lots of artists live paycheck to paycheck. And the thing I've noticed, lots of artists live paycheck to paycheck no matter how much they're making. I knew an animator at Disney who got laid off in the Great Bloodletting of 2002, when the last of the traditional animation staff was given its walking papers. He'd worked at Disney for over twenty years, made sizable bonuses, made big money in the last nine or ten years of his tenure. And within six months of layoff, finding no work, he was forced to sell his house (which was not small.)

Now, this is crappy, no question about it. But my question is, why would somebody who made steady money for two-plus decades, and beaucoup dollars for the last ten years, have to bail out of his domicile within months? A friend of his told me: "When Bill made more bucks, he spent more bucks. He had a Lexus, he had a monster-size house, he had a collection of artwork and rare comic books and lots of pictures of his trips to Europe. What he didn't have was a bank account."

It's a story I've heard a lot in the course of doing this job. When artists are in the chips, they cash in the red ones, the white ones, the blue ones, and party hearty. And when they're shut out of a place at the table, they have nothing in their metaphorical wallets on which to live. As a supervisor at DreamWorks said five years ago: "I drive a beat-up old Buick. Most of the people in my department are driving Jags and BMWs. They think the big salaries are the normal deal, no matter what I tell them."

Five years later, some of those people are surviving on smaller weekly paychecks in smaller places. Some are out of the business altogether. And renting.

Mind you, I don't wag my wizened finger at any of these folks. Twenty years back, I was just like them. I chased rainbows, I didn't save. I assumed, thirty-year-old idiot that I was, that next week would take care of itself. Now, of course, standing in the wide, sunlit uplands of Wisdom and Total Insight, I can look back at the twisting road behind me and see with crystal clarity the choices I should have made, the investments into which I should have put disposable income.

The reasons I bring this up now is, 1) the American savings rate is below zero, 2) saving is relatively painless if you're smart about it (and we don't necessarily have to mimic the American savings rate), and 3) when you reach middle age, you are going to wish like hell you had some cushion of savings to bounce along on.

The first order of business is to start saving. Put something into a 401(k) Plan (the Feds give you a tax break now to do it), then a Roth-IRA (the Feds give you a tax break later), then a certificate of deposit (the Feds give you nothing, but put the money aside anyway). Fund your accounts automatically, on the day you get paid. Set aside a percentage. Pretend the money isn't there.

Learn something about making investments. It isn't particularly hard, and if you're smart about it, the task won't take big amounts of time. Yesterday in the Wall Street Journal there was a column touting investment books; we give you three that are quite good below (two of the three are quick reads):

"Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor," by John Bogle (John Wiley and Sons, Inc.) This book from the former Vanguard chief provides good basics on how to think about mutual fund investing. Mr. Bogle, naturally, favors the indexing strategy that made Vanguard famous, while touching on other aspects of fund investing such as long-term planning, asset allocation and proper risk taking.

The Intelligent Investor Revised Edition," by Benjamin Graham and Jason Zweig. (Collins Business Essentials.) Mr. Graham is famous for his book "Security Analysis," considered the bible of value investing. This book takes a more Main Street approach and provides excellent pointers on how to approach investing. Warren Buffett is one of the many Graham admirers in the investment firmament. Mr. Zweig, a Money Magazine writer, updates this classic with modern examples that outline Mr. Graham's still salient points.

The Little Book that Beats the Market," by Joel Greenblatt (Wiley). If you are looking for a quick investing read, this is for you, since it is, in fact, little. Mr. Greenblatt, a successful hedge fund manager, provides a sharply written, anecdote rich, easy-to-understand investing strategy that any junior high-schooler would understand. While the book boasts a "magic formula," it is basically a reiteration of an age-old theme: Smart investors buy good companies cheaply...

Twenty-plus years ago, I attended one of the Animation Guild's Golden Awards banquet, a ceremony where TAG celebrates artists who have worked fifty years (or close to) in the cartoon biz. While I was standing in the restaurant foyer congratulating a recipient on his fifty years, Disney veteran Joe Hale walked up and said: "Fifty years? This is the only business where you have to work fifty years. To survive..."

Two decades further on, I've come to see what Joe meant...

The animation business can be cold, cruel and abrupt. You're cruising along earning a good salary, happy with your job, thinking it's going to go on forever (or at least until next March) when you get called into a group meeting and told the project's shutting down and everyone will be laid off on Friday (except for Doris the production manager, who's "family.")

And suddenly you're out of work and scrambling. Two weeks before your unemployment runs out, you land another gig at a smaller studio for three hundred less per week, but you're happy to get it. You dig in and give the job your all. And eight months later, the job ends and you're looking for work again.

This, with some variations and exceptions, is the animation industry as many of us know it. Big salaries morph to smaller salaries. Long-term staff employment is followed by a year of free-lance work, then staff work opens up again and wages creep up a bit.

Through it all, lots of artists live paycheck to paycheck. And the thing I've noticed, lots of artists live paycheck to paycheck no matter how much they're making. I knew an animator at Disney who got laid off in the Great Bloodletting of 2002, when the last of the traditional animation staff was given its walking papers. He'd worked at Disney for over twenty years, made sizable bonuses, made big money in the last nine or ten years of his tenure. And within six months of layoff, finding no work, he was forced to sell his house (which was not small.)

Now, this is crappy, no question about it. But my question is, why would somebody who made steady money for two-plus decades, and beaucoup dollars for the last ten years, have to bail out of his domicile within months? A friend of his told me: "When Bill made more bucks, he spent more bucks. He had a Lexus, he had a monster-size house, he had a collection of artwork and rare comic books and lots of pictures of his trips to Europe. What he didn't have was a bank account."

It's a story I've heard a lot in the course of doing this job. When artists are in the chips, they cash in the red ones, the white ones, the blue ones, and party hearty. And when they're shut out of a place at the table, they have nothing in their metaphorical wallets on which to live. As a supervisor at DreamWorks said five years ago: "I drive a beat-up old Buick. Most of the people in my department are driving Jags and BMWs. They think the big salaries are the normal deal, no matter what I tell them."

Five years later, some of those people are surviving on smaller weekly paychecks in smaller places. Some are out of the business altogether. And renting.

Mind you, I don't wag my wizened finger at any of these folks. Twenty years back, I was just like them. I chased rainbows, I didn't save. I assumed, thirty-year-old idiot that I was, that next week would take care of itself. Now, of course, standing in the wide, sunlit uplands of Wisdom and Total Insight, I can look back at the twisting road behind me and see with crystal clarity the choices I should have made, the investments into which I should have put disposable income.

The reasons I bring this up now is, 1) the American savings rate is below zero, 2) saving is relatively painless if you're smart about it (and we don't necessarily have to mimic the American savings rate), and 3) when you reach middle age, you are going to wish like hell you had some cushion of savings to bounce along on.

The first order of business is to start saving. Put something into a 401(k) Plan (the Feds give you a tax break now to do it), then a Roth-IRA (the Feds give you a tax break later), then a certificate of deposit (the Feds give you nothing, but put the money aside anyway). Fund your accounts automatically, on the day you get paid. Set aside a percentage. Pretend the money isn't there.

Learn something about making investments. It isn't particularly hard, and if you're smart about it, the task won't take big amounts of time. Yesterday in the Wall Street Journal there was a column touting investment books; we give you three that are quite good below (two of the three are quick reads):

"Common Sense on Mutual Funds: New Imperatives for the Intelligent Investor," by John Bogle (John Wiley and Sons, Inc.) This book from the former Vanguard chief provides good basics on how to think about mutual fund investing. Mr. Bogle, naturally, favors the indexing strategy that made Vanguard famous, while touching on other aspects of fund investing such as long-term planning, asset allocation and proper risk taking.

The Intelligent Investor Revised Edition," by Benjamin Graham and Jason Zweig. (Collins Business Essentials.) Mr. Graham is famous for his book "Security Analysis," considered the bible of value investing. This book takes a more Main Street approach and provides excellent pointers on how to approach investing. Warren Buffett is one of the many Graham admirers in the investment firmament. Mr. Zweig, a Money Magazine writer, updates this classic with modern examples that outline Mr. Graham's still salient points.

The Little Book that Beats the Market," by Joel Greenblatt (Wiley). If you are looking for a quick investing read, this is for you, since it is, in fact, little. Mr. Greenblatt, a successful hedge fund manager, provides a sharply written, anecdote rich, easy-to-understand investing strategy that any junior high-schooler would understand. While the book boasts a "magic formula," it is basically a reiteration of an age-old theme: Smart investors buy good companies cheaply...

A book that I found real useful is a volume titled The Truth About Money," by Ric Edelman. He pretty much covers everything about the long green that you'll need to know, and he's simple, clear and direct, plus his investment tips are good. (We give you one of his investment charts to the left -- which is self-explanatory, I think. DI-VERS-IFY)

The point is, no matter where you are with your career, you need to pay attention to saving for retirement (And to what you've already got. Cases in point: In the last couple of months, I've encountered several animation artists who've worked fifteen-plus years in signator shops that were astounded to learn that they get TWO pensions automatically. Most kew about the monthly benefit check they get, but they didn't know they get a BIG retirement lump-sum payment when they retire called The Individual Account Plan. They were delighted they had sixty thousand dollars sitting in an account in their name. I was surprised they didn't know...)

Moral of the story: start saving early. Even if it's a pittance, be consistent about it. By the time you reach fifty or sixty, you won't be worrying about what you'll do for eating money when your last employer waves you out the door into the waiting arms of Social Security.

A book that I found real useful is a volume titled The Truth About Money," by Ric Edelman. He pretty much covers everything about the long green that you'll need to know, and he's simple, clear and direct, plus his investment tips are good. (We give you one of his investment charts to the left -- which is self-explanatory, I think. DI-VERS-IFY)

The point is, no matter where you are with your career, you need to pay attention to saving for retirement (And to what you've already got. Cases in point: In the last couple of months, I've encountered several animation artists who've worked fifteen-plus years in signator shops that were astounded to learn that they get TWO pensions automatically. Most kew about the monthly benefit check they get, but they didn't know they get a BIG retirement lump-sum payment when they retire called The Individual Account Plan. They were delighted they had sixty thousand dollars sitting in an account in their name. I was surprised they didn't know...)

Moral of the story: start saving early. Even if it's a pittance, be consistent about it. By the time you reach fifty or sixty, you won't be worrying about what you'll do for eating money when your last employer waves you out the door into the waiting arms of Social Security.

6 comments:

Job Security, or, the lack there of, is something schools are not teaching the students, and how to cope with it.

And yet, kids, these days seem well prepared in other areas. Lots of them have their own websites when they graduate! when I graduated, I did'nt even know what e-mail was !! (yahoo was a few years old at the time!)

I lost a buch of money on some poor investments, during the tech bubble in the nineties.

Should have done more research!

I wish you'd address the persistence of ageism in the entertainment industry (and, by extension, in animation). It may or may not be a little better in feature animation, but as a salt-miner in the television trenches, there are very few directors in their fifties, and next to none in their sixties.

So any retirement planning has to take into consideration that you may be unemployable in the industry earlier than you may expect...

All the more reason to save your money. This is not just an animation concern, the entire entertainment industry is currently obsessed with youth.

When I came into the business, all my bosses were old codgers -- animation veterans. Today, a veteran could very well be in his or her twenties. Like it or not, I don't think it's going to change anytime soon.

If you're unlucky enough to be an aging veteran, put that experience to work in other areas. Those years working in the business can still count. There are options other than working in the mainstream studios.

Its true that the studios attitude changes when they start seeing the grey hair. When I got in the business silver locks meant you had made it, like Frank & Ollie. Now that I'm sprouting grey hair someone changed the rules on us! Now you're thought of as overpaid and out of ideas.

The most important thing I discovered when I was president was the number of animation "celebrity" types who despite their fame depended upon the 839 pension to support them. MGM didn't make Hanna & Barbera rich for making them all those wonderful Tom & Jerrys, Warners didn't make Chuck Jones rich for creating Roadrunners for them. They got straight salary like the rest of us. They made their fortunes afterwards as independents.

But if you don't want to go the Donald Trump route, then stick with your union gigs or do something about your retirement. I wish I could be Joe Grant or Al Hirshfeld and draw until I'm 100 and die at my desk, but the odds of that are unlikely.Think of yourself like a ballplayer. The nestegg you make now will keep you when it's time to hang the jersey up.

This job of business rep gives you a bird's eye view of the smart (and stupid ) things people in our industry do.

I know artists in their sixties and seventies who have Social Security, and that's about it. They never saved, they seldom worked a union gig, and now, as the saying goes, the Rhode Island Reds have come home to roost.

I know artists in their forties and fifties who were in the right place at the right time during the nineties animation boom, and are now set for life. (Can we say, "Disney Feature Animation"? Can we say "bonuses"? I'll bet we can.)

And I know older artists who SHOULD be okay, but have made one stupid move after another, and now have to scramble. (Case in point: a sixty-eight-year old artist had a pension coming at 65, but failed to contact the plan. His son and daughter called the office to find out if there was any way he could go back and get those monthly checks he never got because he didn't fill out an application in a timely manner. I had to tell them "no." On industry pensions, there is no retroactivity. You gotta ask for it to get it.)

Wow- That was depressing.

Post a Comment